(with Ronel Elul and Şebnem Kalemli-Özcan)

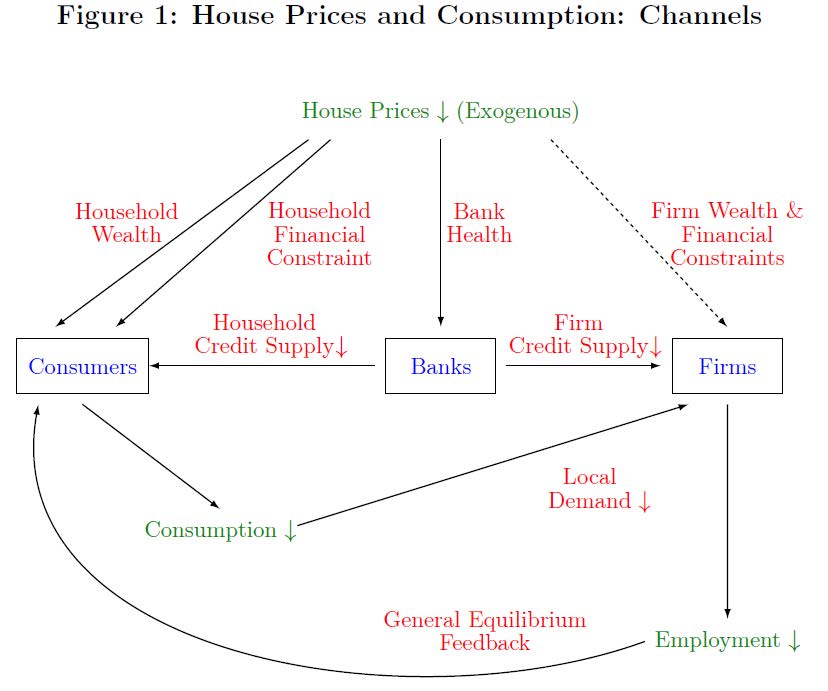

We quantify the role of heterogeneity in households’ financial constraints in explaining the large decline in aggregate consumption between 2006 and 2009 using individual-level data. Financial constraints can explain 56\% of the aggregate response of consumption to changes in house prices. Local general equilibrium feedback and decline in bank credit to consumers make up the remaining 44%. Our results show that a large part of the response that was attributed to wealth effects in the prior literature, can in fact be explained by heterogeneity in households’ financial constraints.

First draft : March 2018

Paper

Most Recent Working Paper [January 2024]