(with Jesus Fernandez-Villaverde and Juan F. Rubio-Ramirez)

Published in Journal of Economic Dynamics and Control, December 2006, 30(12), 2477-2508.

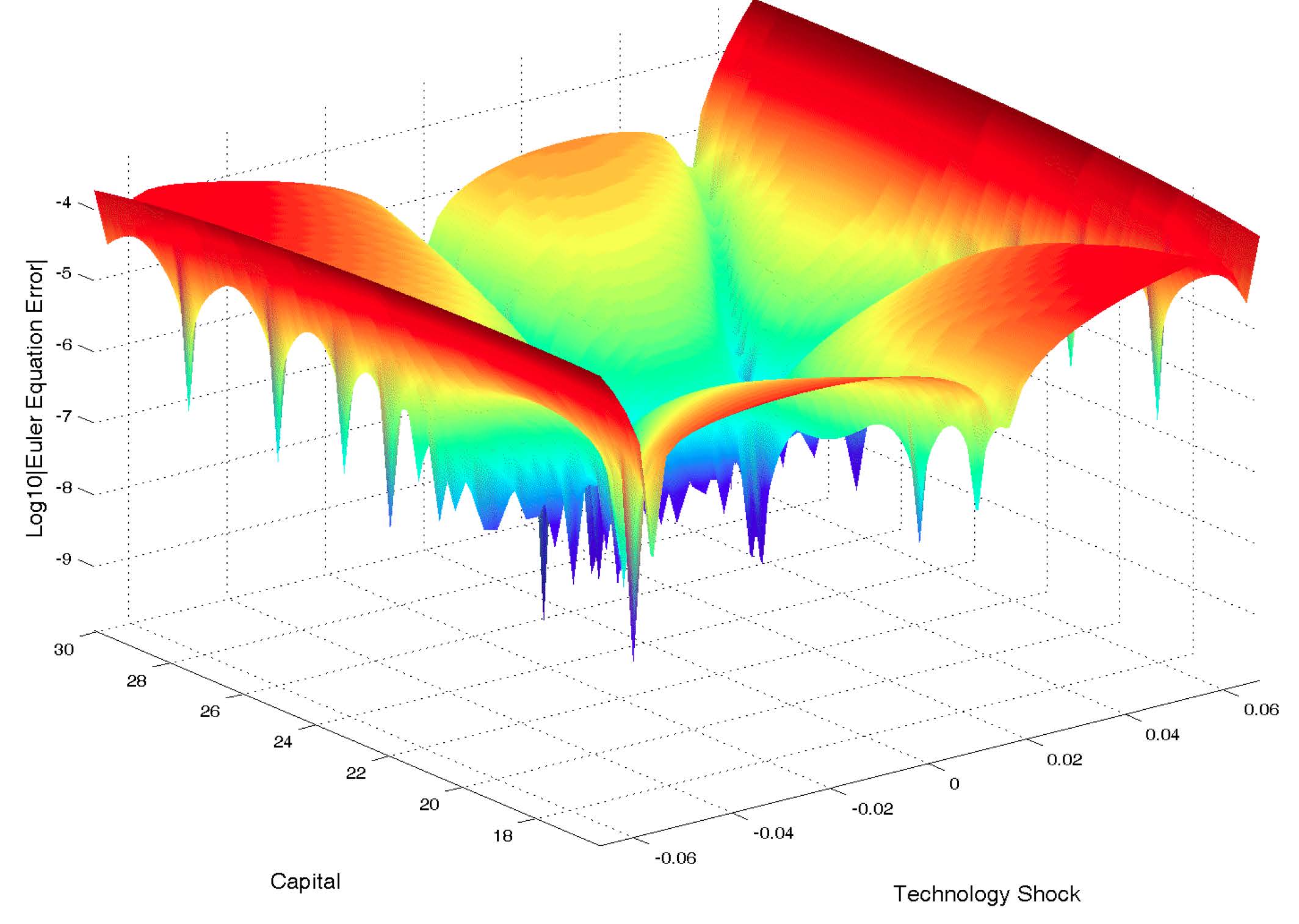

This paper compares solution methods for dynamic equilibrium economies. We compute and simulate the stochastic neoclassical growth model with leisure choice using first, second, and fifth order perturbations in levels and in logs, the finite elements method, Chebyshev polynomials, and value function iteration for several calibrations. We document the performance of the methods in terms of computing time, implementation complexity, and accuracy, and we present some conclusions based on the reported evidence.

Paper

Most Recent Working Paper (may not be identical to the published version)

Published Version (requires subscription)

Additional Materials

Companion Webpage (includes codes and an extended working paper)