(with Francis X. Diebold and Glenn D. Rudebusch)

Published in Journal of Econometrics, March-April 2006, 131(1-2), 309-338.

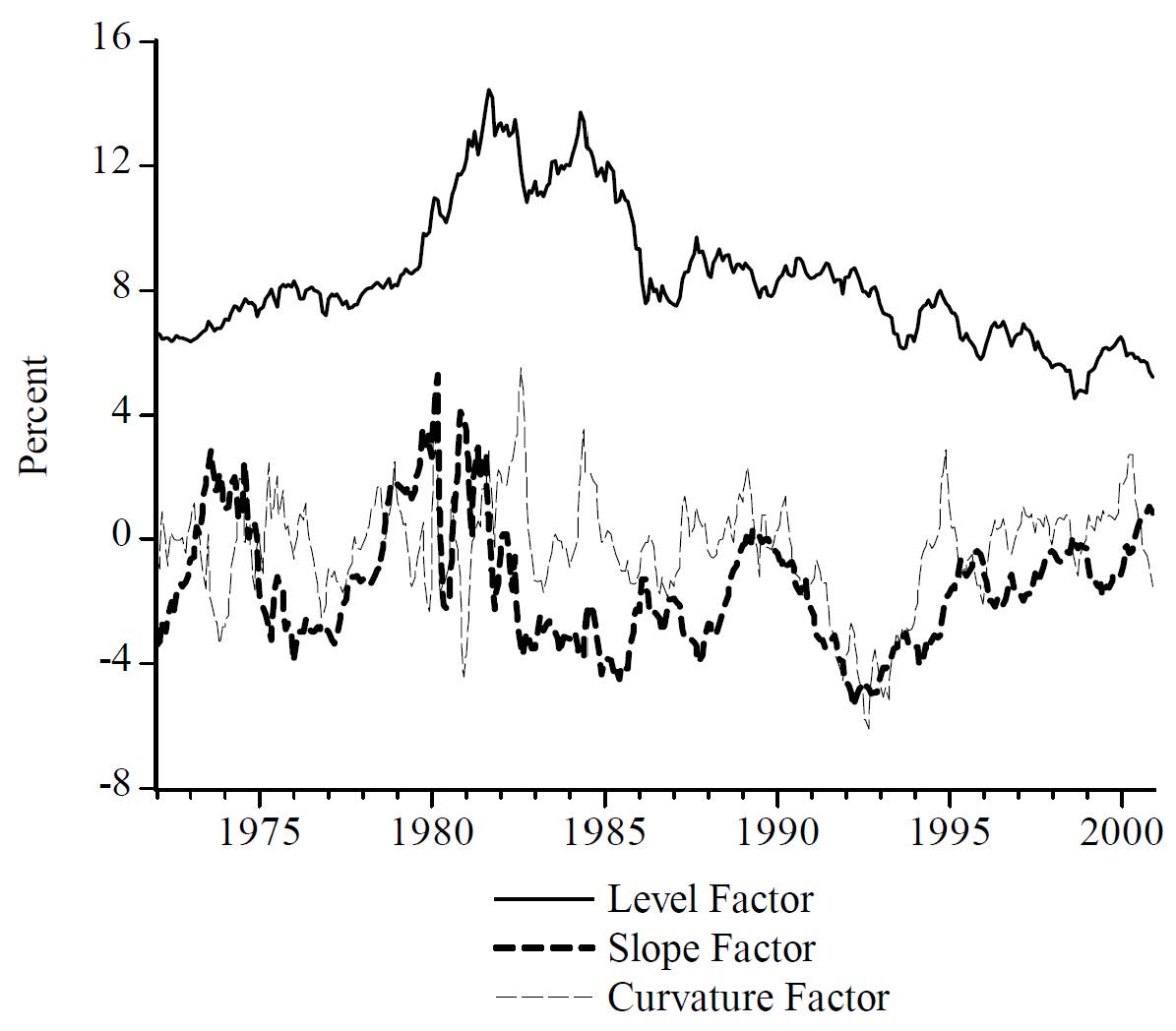

We estimate a model that summarizes the yield curve using latent factors (specifically, level, slope, and curvature) and also includes observable macroeconomic variables (specifically, real activity, inflation, and the monetary policy instrument). Our goal is to provide a characterization of the dynamic interactions between the macroeconomy and the yield curve. We find strong evidence of the effects of macro variables on future movements in the yield curve and evidence for a reverse influence as well. We also relate our results to the expectations hypothesis.

Paper

NBER Working Paper 10616 [July 2004]

Most Recent Working Paper (may not be identical to the published version)

Published Version (requires subscription)

Additional Materials

Data Used in the Paper (text file)

RATS code that replicates the results of the paper (Written by Tom Doan from Estima — offered here with no warranties)