(with Francis X. Diebold and Chiara Scotti)

Published in Journal of Business and Economic Statistics, 2009, 27(4), 417-427 (lead article).

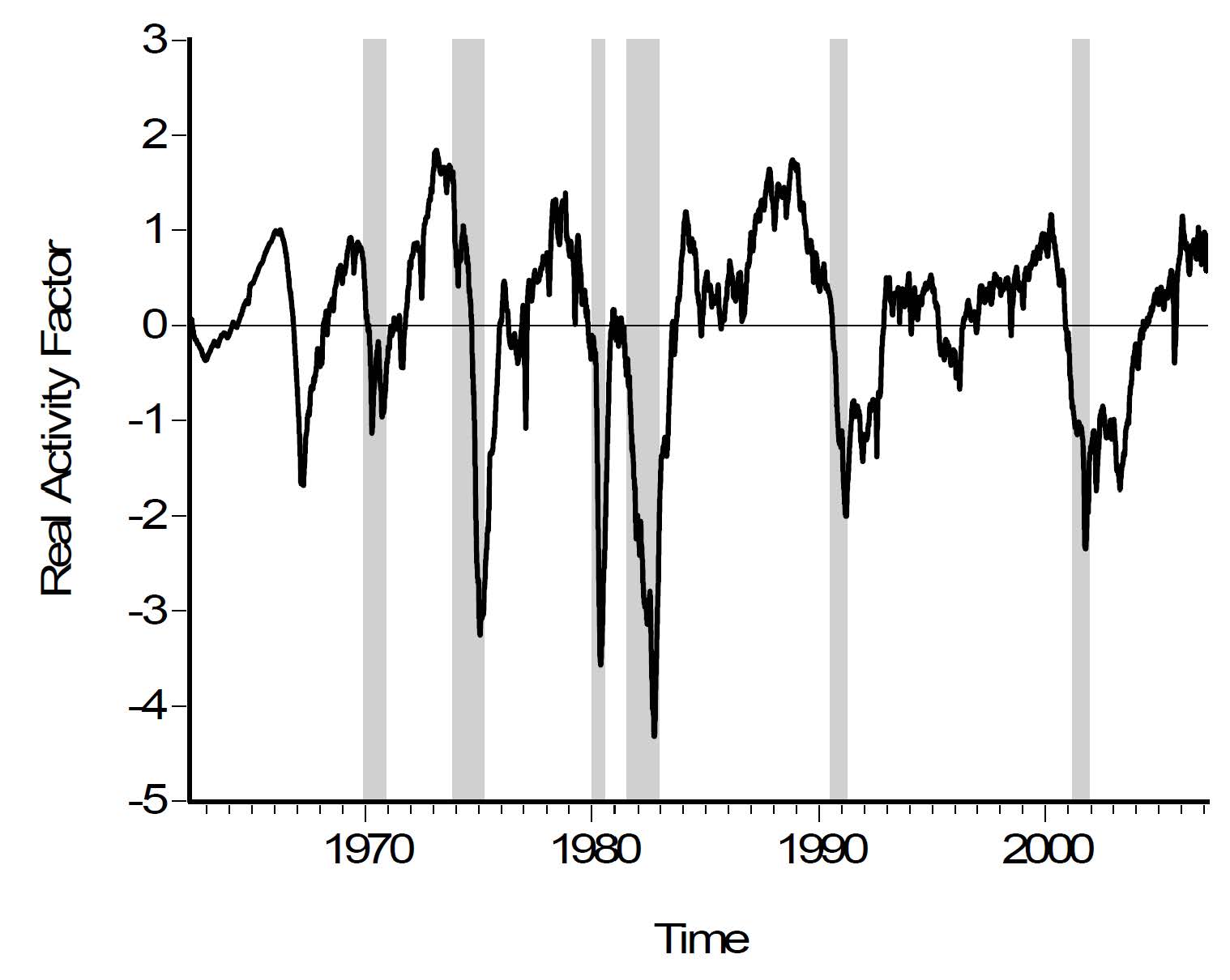

We construct a framework for measuring economic activity at high frequency, potentially in real time. We use a variety of stock and flow data observed at mixed frequencies (including very high frequencies), and we use a dynamic factor model that permits exact filtering. We illustrate the framework in a prototype empirical example and a simulation study calibrated to the example.

First Draft : March 2007

As of January 9, 2009, the Federal Reserve Bank of Philadelphia started producing the Aruoba-Diebold-Scotti Business Conditions Index based on the methods developed in this paper.

Paper

NBER Working Paper 14349 [September 2008]

Most Recent Working Paper (may not be identical to the published version)

Published Version (requires subscription)

Additional Materials

Press Mentions

Dow Jones Newswires [January 9, 2009]

The Press of Atlantic City [January 11, 2009]

Philadelphia Inquirer [January 15, 2009]

Econ Browser (James Hamilton’s Blog) [April 15, 2009]

Capital Spectator [November 20, 2009]

Philadelphia Inquirer [January 29, 2010]